Markets on the Precipice: The Tariff Saga Continues

Welcome back, dear readers, to our attempt to make sense of this market that's been trying very hard to convince us it's fine while occasionally breaking into cold sweats.

We've been on quite the roller coaster these past few weeks. First, we had President Trump's "Liberation Day" announcement that sent markets into a tailspin faster than you could say "reciprocal tariffs." Then, as if the market gods decided we'd had enough character-building for one month, a 90-day reprieve appeared and sparked one of the best single-day rallies for Nasdaq and the S&P in history.

Now we're in that curious state of financial limbo that markets occasionally find themselves in — things aren't great, but they're maybe a little better than the catastrophe we briefly priced in. It's like when your doctor says, "Well, it's not the bad kind of tumor," and you're simultaneously relieved and horrified to learn there was a tumor at all.

Let's pull apart what's happening and what it might mean for your portfolio, your retirement, and your general sense of financial well-being over the coming months.

The Tariff Saga: From Terrifying to Merely Frightening

The Trump administration has begun walking back some of its most aggressive tariff policies, like a diner who ordered the extra spicy wings and is now quietly asking for more ranch dressing. The 90-day pause of "reciprocal" tariffs and exemptions for ICT products from China tariffs were just the appetizers. Recently, the White House modified auto parts tariffs to prevent "stacking" with steel/aluminum tariffs and partially reimburse automakers.

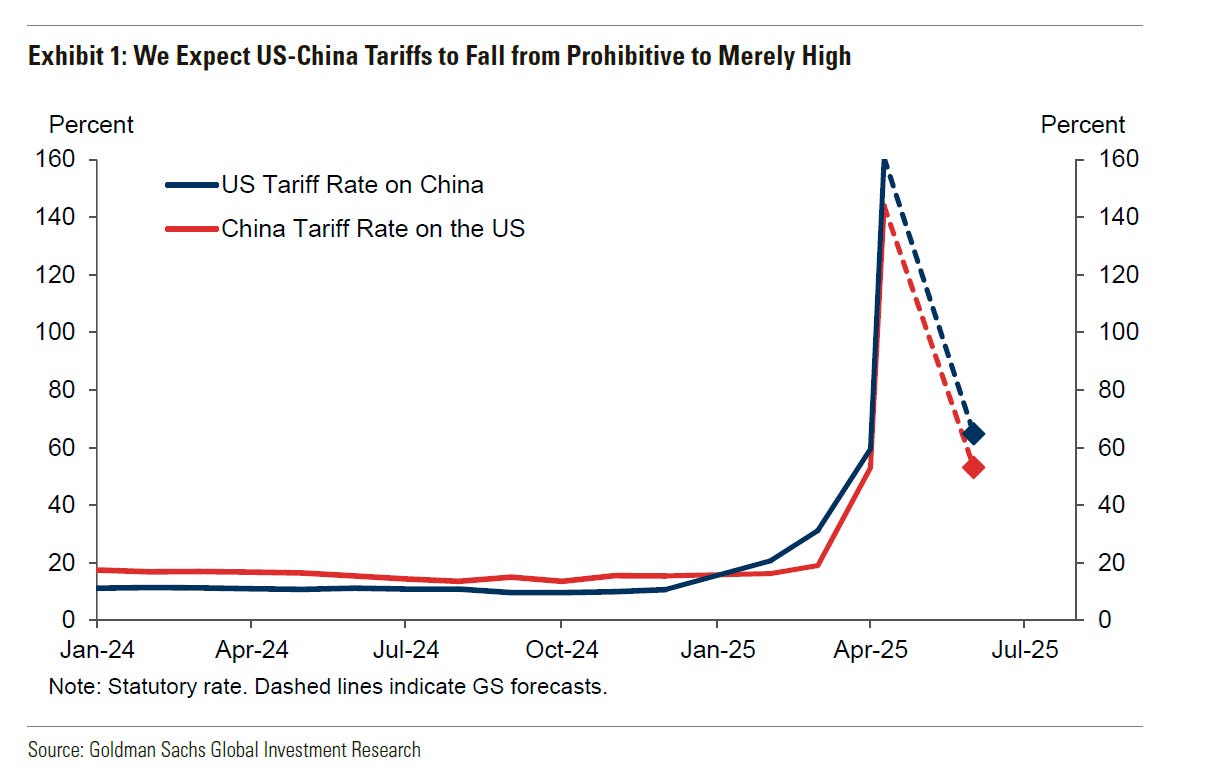

The mood music with China has improved too. Goldman's economists expect US tariff rates on China to drop from around 160% (think "no trade allowed whatsoever") to around 60% (think "painful but possible") relatively soon. China will likely reduce its tariffs on the US by a similar amount.

That's not free trade, but it's less apocalyptic than what was briefly feared in early April. The market equivalent of going from "We're all going to die!" to "Many of us will survive, but with significant injuries."

But here's the thing about tariffs—even at "only" 60%, they remain a significant impediment to trade. It's like saying your commute isn't so bad because it's only a 60% chance of gridlock every day. And beyond US-China, we should expect further tariff increases in other areas like pharmaceuticals, semiconductors, and potentially movies. (Nothing says "America First" like making sure American consumers pay more for medicine and semiconductor-powered devices, I suppose.)

These tariffs aren't just about slightly more expensive consumer goods. At these levels, they fundamentally reshape supply chains, corporate planning, and investment decisions. It's not just paying a bit more for your iPhone; it's Apple potentially rethinking how and where it manufactures everything. Multiply that across thousands of companies and you get economic growth that looks very different than what we've been used to.

The Deceptive Calm of Hard Data

Friday's jobs report looked fine, like that friend who assures you they're "totally okay" right after a breakup. Initial jobless claims, adjusted for seasonal distortions, indicate continued resilience in the labor market. But does this mean the economy is truly dodging a bullet?

Not necessarily. As Goldman points out, hard economic data tends to lag significantly in event-driven downturns like what we're experiencing now. The surge in pre-buying that occurred ahead of tariff implementation (businesses stocking up before prices rise) likely extends that lag further. It's like how you don't feel the sunburn until hours after you've left the beach.

The soft data—which has its own shortcomings but is less susceptible to pre-buying distortions—has already fallen more than in the typical event-driven recession. This is especially true for consumer and business expectations. People and businesses aren't waiting for the official recession announcement to start feeling pessimistic.

In other words, the foundation is cracking even if the visible structure still looks intact. It's the economic equivalent of those cartoons where the character has run off a cliff but hasn't looked down yet.

Central Banks: The Reluctant Firefighters

Central banks are in a tricky position, like someone trying to decide whether to deploy the fire extinguisher while the curtains are smoldering but not yet fully ablaze.

The Federal Reserve, that bastion of carefully worded ambiguity, has pushed back the timeline for rate cuts from June to July in Goldman's baseline. While the Fed won't be swayed by presidential tweets or criticism (at least that's what they tell themselves in the mirror each morning), there are more fundamental concerns about its independence. If the White House gains the ability to remove FOMC members without "cause"—defined as inefficiency, neglect of duty, or malfeasance in office—the Fed would become a negative outlier among developed market central banks. Academic studies show that reduced independence predicts worse inflation outcomes over time, which is a fancy way of saying "politics and stable prices don't mix well."

In Europe, central banks are taking divergent approaches, like siblings who grew up in the same household but developed radically different personalities. The ECB remains relatively dovish, with expectations for three more sequential 25bp cuts to 1.5% despite modest improvement in manufacturing PMIs. The risks are tilted toward bigger and/or deeper cuts.

The Bank of England surprised on the hawkish side, with two members preferring to keep rates unchanged at the last meeting. Even the majority who voted for a cut were apparently wavering. It's the central banking equivalent of ordering a diet soda with your triple cheeseburger—a halfhearted gesture toward restraint.

The Bank of Japan has delayed its next expected rate hike by six months to January 2026, responding to trade policy uncertainty. However, the terminal policy rate forecast of 1.5% remains unchanged, as wage growth and inflation expectations remain encouraging. Japan, as always, continues to be a world unto itself.

What This Means for Your Portfolio (And Your Sanity)

Asymmetric Risk in Equities

The asymmetry for equity investing looks poor right now. Sharp rallies within bear markets are the norm, not the exception—like those sunny days in the middle of winter that trick the flowers into blooming early. Retail buyers have been "buying the dip," but positioning isn't extreme enough to suggest a contrarian bullish signal.

While hard data has generally held up and Q1 earnings have been relatively healthy, much of this is backward-looking. It's like judging your car's condition by looking in the rearview mirror while there's smoke coming from under the hood.

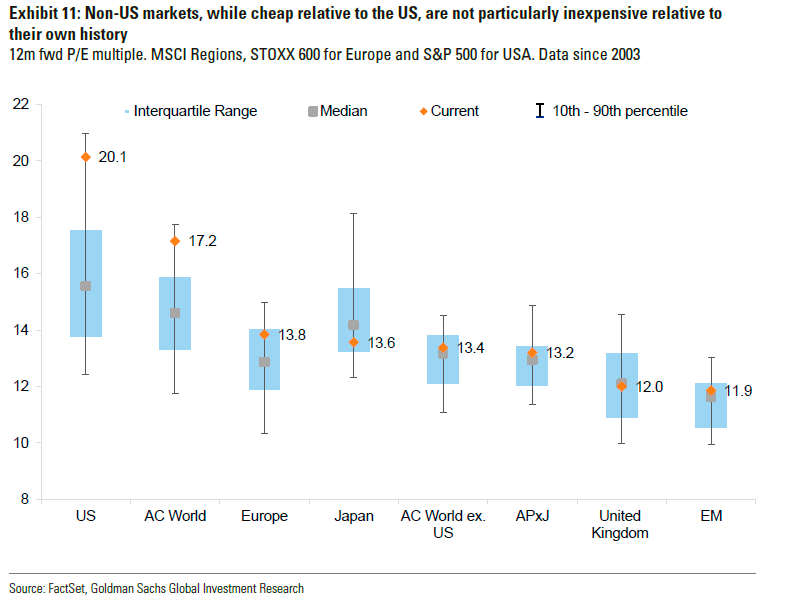

The more interesting story is about US exceptionalism—the extraordinary outperformance of US assets relative to the rest of the world that's been the defining market narrative for nearly 15 years. Foreign investors have been willing buyers of dollars and US assets, attracted by a dynamic economy and technology sector. This has pushed the dollar to a two standard deviation premium to its long-term fair value and US equity valuations above their 90th percentile of historic ranges.

But in a less globalized world with higher capital costs and government debt, it's not clear the US advantage remains as strong. New competition in AI, coupled with higher capital employed by US tech giants, might erode relative returns. The market equivalent of realizing that your straight-A student might not actually be that much smarter than their peers—they just had better tutors and resources.

The data suggests that while US companies have consistently achieved higher margins and ROE compared to competitors in the same industry elsewhere, the gap began to exceed what was justified by fundamentals in 2024, just as the belief in "US exceptionalism" was gaining currency. That's usually when narratives start to unravel.

Interest Rates: Waiting Game

Rates markets are in a peculiar position, like a chess player who sees several possible moves but isn't sure which one leads to checkmate and which one to disaster. Wednesday's Fed decision didn't provide much direction, but did offer some guideposts. "Wait and see" is the operative phrase, but even with acknowledged upside risks to near-term inflation, the assessment that most longer-term expectations remain consistent with the 2% target suggests the hawkish risk is more about an extended hold than a resumption of hikes.

The bar to cuts is higher than in 2019 and depends on observable deterioration in hard data. With sufficient evidence of weakness currently absent, there's risk that markets continue to price out cuts. Such a shift would likely come from trimming the left tail around the policy rate path rather than the sort of acute flattening pressure that a repricing of the right tail would bring.

In human language: The Fed will cut rates if things get bad, but "bad" now has a higher threshold than before, and the market is still figuring out what that means.

This creates a window to earn some carry (like in 3y swap spreads or front-end roll-up trades), with a core steepening bias effectively acting as a long volatility overlay. If that sentence made your eyes glaze over, just know that there's an opportunity to make some relatively safe money while waiting for clearer signals.

Sovereign Credit Over Core Rates

In Europe, with core rates trading alongside improving global risk sentiment and cautious central bank communication, it's becoming difficult to sustain cut pricing without clear deterioration in hard data. ECB cut pricing out to September is now below 50bp, whereas Goldman's economists expect 75bp of cuts over that period, suggesting improving risk-reward for longs.

But given the relative symmetry in terminal rate pricing and the fact that fiscal expansion is likely to support higher Bund yields over time (forecasted at 2.80% by end-2025), sovereign credit longs look more attractive than core rates.

The Wild Card: Dutch Pension Reform (Yes, Really)

Sometimes the most important market shifts come from the places you least expect. Enter Dutch pension reform—the market equivalent of the shy person at the party who turns out to have the most interesting stories.

The transition of the Dutch pension fund industry from defined benefits toward collective defined contribution remains in focus for European rates markets. This reform is expected to weaken incentives for pension funds to hedge their interest rates exposure through swap receivers, especially at the very long-end of the curve.

Translation: One of the largest pools of European investment capital is changing how it operates, and this will affect interest rates across the continent in ways that create potential trading opportunities.

It's also likely that pension funds will have less need to add to duration longs following rallies, and lower use of long-end swaps may mean less safe asset liquidation to meet margin calls following sell-offs.

Long-end curve steepeners (such as 10s30s) look like the cleanest expression to position for this transition, as it aligns with the broader macro backdrop. It's like noticing that a massive cargo ship is slowly changing course and positioning yourself to benefit from the wake.

Trading Ideas Worth Actually Considering

Based on all this analysis, here are some potentially interesting trade ideas. As always, I've tried to separate the signal from the noise—the financial equivalent of telling you which items from the buffet probably won't give you food poisoning:

1. Long 3y SOFR-UST swap spreads

The dramatic tightening in US swap spreads since early April has taken spreads to levels that screen cheap relative to fair value. The resilience of belly and long-end spreads despite refunding auctions is noteworthy.

This is a bit like noticing that a typically expensive restaurant has suddenly started offering a prix fixe menu at a substantial discount. The quality hasn't changed, just the price.

2. Long 30y TIPS vs. short 0.75x 30y nominal USTs

Inflation forwards have compressed by more than justified by growth and policy reassessments. Relaxation about growth concerns and market functioning could see forward inflation reprice higher, especially in the long end.

This trade is essentially saying: "The market is too confident that long-term inflation is dead." Given the structural inflationary pressures from deglobalization, higher fiscal deficits, and the green transition, that confidence seems misplaced.

3. 10s30s EUR OIS curve steepeners

Dutch pension reform creates a long-term structural case for steepening. This trade aligns with the broader macro backdrop and Goldman's curve model signals.

Sometimes the most profitable trades come from understanding plumbing rather than grand macroeconomic theories. This is one of those cases.

4. Long 3m10y USD payer on the 3m 5s10s30s payer fly

A low-cost way to have exposure to higher yields and term premium risks. Provides some protection against a scenario where we see fiscal sustainability concerns without Fed relief.

This is like buying relatively cheap insurance against a scenario that's becoming increasingly plausible—the market equivalent of noticing that hurricane insurance is underpriced even as storm clouds gather on the horizon.

5. Diversify more by region, sector and factor

The case for diversification remains very strong. The opportunity cost to generate alpha rather than beta continues to rise.

After years of "just buy US tech stocks" working as an investment strategy, we may be entering a period where thoughtful diversification matters again. It's like realizing that the party with the free-flowing champagne is winding down, and it might be time to plan for a more varied diet.

6. SEK belly positions

The belly has underperformed on the 2s5s10s fly year-to-date. Hard data resilience and potential reprieve on tariff news suggest more balanced front-end risks.

Sometimes opportunities emerge simply because everyone is looking elsewhere. While traders focus on the US, Europe, and China, smaller markets like Sweden offer interesting value.

7. Positive on UK long-end rates

Doubts about the tariff-induced growth hit mean near-term upside risks to yields. However, downside risks to activity, coupled with inflation progress and the hawkish BoE, should support long-end outperformance.

The UK, in its post-Brexit identity crisis, continues to march to its own drummer—creating opportunities for those willing to understand its particular rhythms.

The Bottom Line

This is a tricky time for investors—like trying to navigate a mountain road in fog. While the economy has held up better than expected so far, risk asset markets have already taken a lot of credit for this modest surprise. Further relaxation is possible, especially if trade deals materialize over the next few weeks, but it's risky to chase the rally on the eve of what still looks likely to be significant price hikes, supply chain disruptions, and job losses.

Goldman's economists still put 12-month recession risk at 45%, which is...not great. It's like your doctor saying there's a 45% chance you'll need major surgery within a year. You might want to prepare for that possibility rather than booking non-refundable vacations.

The strongest views across markets remain a weaker dollar and higher gold prices. Beyond these, UK rates, copper, and US natural gas look bullish, while oil appears bearish.

Two well-established rules in equity investment have lost relevance in recent years: diversification improves risk-adjusted returns, and profits and margins mean-revert over the long run. For many years after the financial crisis, unique conditions undermined these principles.

But now? The pendulum may be swinging back. While the US isn't likely to enter a secular period of underperformance or see a significant fall in ROE, the gap in returns between the US and other markets, particularly in dollar terms, will likely fade.

The best approach may be to rebalance portfolios to reflect the longer-term opportunities of mean reversion in both returns and valuations. We're not at the apocalypse that was briefly priced in, but we're not in the clear either. We remain, as the title suggests, on the precipice of change.

As Warren Buffett often says, "Be fearful when others are greedy, and greedy when others are fearful." The problem is that right now, the market seems to be oscillating between fear and greed on a daily basis. Perhaps the true wisdom is in recognizing that both emotions are currently justified—and positioning accordingly.

Disclaimer: This article is based on research reports but represents my own analysis and interpretations. This content is for informational purposes only and does not constitute investment, legal, or tax advice. The views expressed are my own and do not represent the opinions of any research provider or any other institution. All investments involve risk, including the possible loss of principal. Past performance is not indicative of future results. Market conditions change rapidly, and the information presented may be outdated by the time you read it. Before making any investment decision, you should conduct your own research, consider your financial situation, risk tolerance, time horizon, and investment objectives, and consult with qualified financial, legal, and tax professionals. The author may hold positions in securities mentioned in this article. This is not an offer to sell or solicitation of an offer to buy any securities.